If you're in your 20s, you've probably seen stock financial advice like this before.

- live within your means i.e. budget

- save and invest your money as fast as you can

- and take care of your health by staying active.

These tips can put anyone on a strong financial footing later in life, but all-too-often people make costly mistakes like:

- racking up credit card debt

- smoking

- buying a car beyond our means

- choosing a career in a field with too many candidates for too few job openings.

We literally pay for making these kind of irresponsible decisions, and they haunt and follow us around for years – affecting how much things cost.

Put another way:

Doing smart things with your money when you're 25 years-old versus when you're 35 years-old could cost you as much as $1 million bucks.

How is this possible?

Because time works in your favor when you're young and money invested wisely can grow without you having to work.

And each year counts when it comes to investing and your health. A lot.

There are things you can do right nowto start your personal finance journey on the right path, or course-correct if you've already made any missteps.

You don't want to find yourself older wishing you hadn't procrastinated putting money to work for you.

So let's review the best financial advice we've found – because, let's face it, financial tips for young people differ from those in mid-career or closing in on retirement.

You don't want to miss any good opportunities to make the most of time and money, especially when it's working in your favor now.

Just look at the difference a 20-year-old needs to save each month to have $1m at retirement versus what a 40-year-old (who didn't save a penny) needs to put away.

1. Get the right education and get yourself closer to big bucks

The kind of education and training you receive as a young adult can have a significant impact on your earning potential.

It's important to pay attention to not only what's hot right now, but also what fields are likely to experience significant job growth and are not already oversaturated with qualified workers. Do your "homework" accordingly.

Some things to consider:

Earn $15k more with "STEM"

The Department of Education revealed that it expects STEM (science, technology, engineering, and math)-related jobs to increase by 14 percent overall this decade; the outlook for biomedical engineers is the brightest with a 62 percent increase.

Beyond the fact that there are more jobs opening up, the fields are also lucrative.

According to a large Department of Education study, four years after graduation, those who finish college with STEM degrees are earning an annual salary that's $15,500 higher than those with other majors.

If you're still dabbling in your major, or are considering a return to school, take a look at your school's STEM programs to set yourself up for a lucrative career.

Elite schooling doesn't always mean bigger bucks

Analysts from the Wall Street Journal surveyed 7,300 college graduates 10 years after their graduation to figure out whether those who went to highly selective schools earned more than their counterparts at "mid-tier" or less-selective schools.

It turns out that which school you go to makes a difference only in some types of careers.

Simply put, you shouldn't get so hung up on getting into "the top school" if you're pursuing a career in the STEM fields vs. "the right school for you."

You should note, however, that business, social science, and education majors all earn significantly more if they graduate from elite schools. You may want to continue shooting for the stars for those if you're headed down that professional pathway.

Make the most of a two-year associate degree

Four-year school isn't in the cards for everyone, we know. Don't fret!

CareerBuilder has compiled a list of the 10 highest-paying jobs that require an associate degree.

The list may surprise—and encourage—you:

- Air Traffic Controller – $113,547

- Radiation Therapist – $76,627

- Dental Hygienist – $70,408

- Nuclear Medicine Technologist – $69,638

- Nuclear Technician – $68,037

- Nurse – $65,853

- Diagnostic Medical Sonographer – $65,499

- Fashion Designer – $63,170

- Aerospace Engineering and Operations Technician – $61,547

- Engineering Technician (except drafters) – $58,698

The kind of education and training you receive as a young adult can have a significant impact on your earning potential.

Just look at the latest correlation between unemployment rate, earnings, and education published by the Bureau of Labor Statistics:

So what your parents, family, and friends were right: Stay in school, kids!

2. Good habits and choices really pay off

Did your parents ever teach you to divvy up your allowance or birthday money into "save" and "spend" portions? If they did, consider yourself lucky.

Financial literacy is as important as learning how to read. It's a bizarre curiosity that we don't teach this in school.

Fortunately, the skills required to save and budget are not hard to master at all. What's challenging is developing the habits to consistently put them to good use.

The older you are, the harder it is to change your habits, which is why you should get cracking now.

Save the change, and then invest it

If you're paying with cash, one simple way to start saving up is to collect all your coins into a jar that you periodically roll up and turn in at the bank.

At the end of each day, just empty your pockets or purse—but don't go too crazy with the size of your jar.

Change isn't just the jingle jangle in your pocket. Check out Acorns, which rounds up expenses on your credit card into loose "change" and puts the cash into an investment account automatically for you.

Choose the right bank

There can be significant differences in interest rates and fees between banking institutions.

What may seem minimal—a $10 monthly checking account fee, for instance, can put a serious crimp in your savings plan when you start crunching the numbers and realize that's an extra $120 you could have had in your savings account this year.

Don't just consider local banks when looking for a place to stash your cash; also look into credit unions and online-only banks.

The key when comparing banks is to know what to look for and how to avoid making bankers richer at your expense, such as:

- No monthly fee

- No minimum balance required

- No limitations on the number or method of transactions

- Free ATM access

- Online and mobile access

The sooner you start choosing a right bank., the more benefits you'll reap.

3. Take care of your health (healthy body, healthy bank account!)

When you're a young professional, you can feel invincible—and make irresponsible decisions that wreck your health and your savings later.

If you're still staying up and partying too late, putting off doctor's visits, and eating fast food, consider that not only do healthy people usually have to spend less on medical costs, but they also get paid more, according to Money magazine.

The article highlights research that indicates:

- "A full night's sleep has been linked to 5 percent higher pay.

- Regular exercise fattens paychecks by 7 to 12 percent.

- Stressing about money means more sick days from work"

Go to the gym

Not only does exercise help your physical and mental health, but it could lead to lower insurance premiums.

Some insurers, like Kaiser Permanente, are experimenting with group incentive-based wellness programs, and others, like Oscar, offer incentives like Amazon gift cards for meeting step-counting goals each day.

Backing up the claim by Money magazine that regular exercise correlates to higher pay, a Journal of Labor Research report found that workers who exercise regularly earned 9 percent higher pay on average than those who don't.

Lose weight or pay up

Obese adults spend an average of $1,429 more per year in medical expenses compared to adults in normal weight ranges because obesity raises your risk of diabetes, cardiovascular disease, certain cancers, chronic pain, and many other conditions.

Besides the higher medical costs, people with obesity will likely pay more for health and life insurance, due to their higher risk of requiring medical care.

The USDA offers strategies to help you get started with weight management.

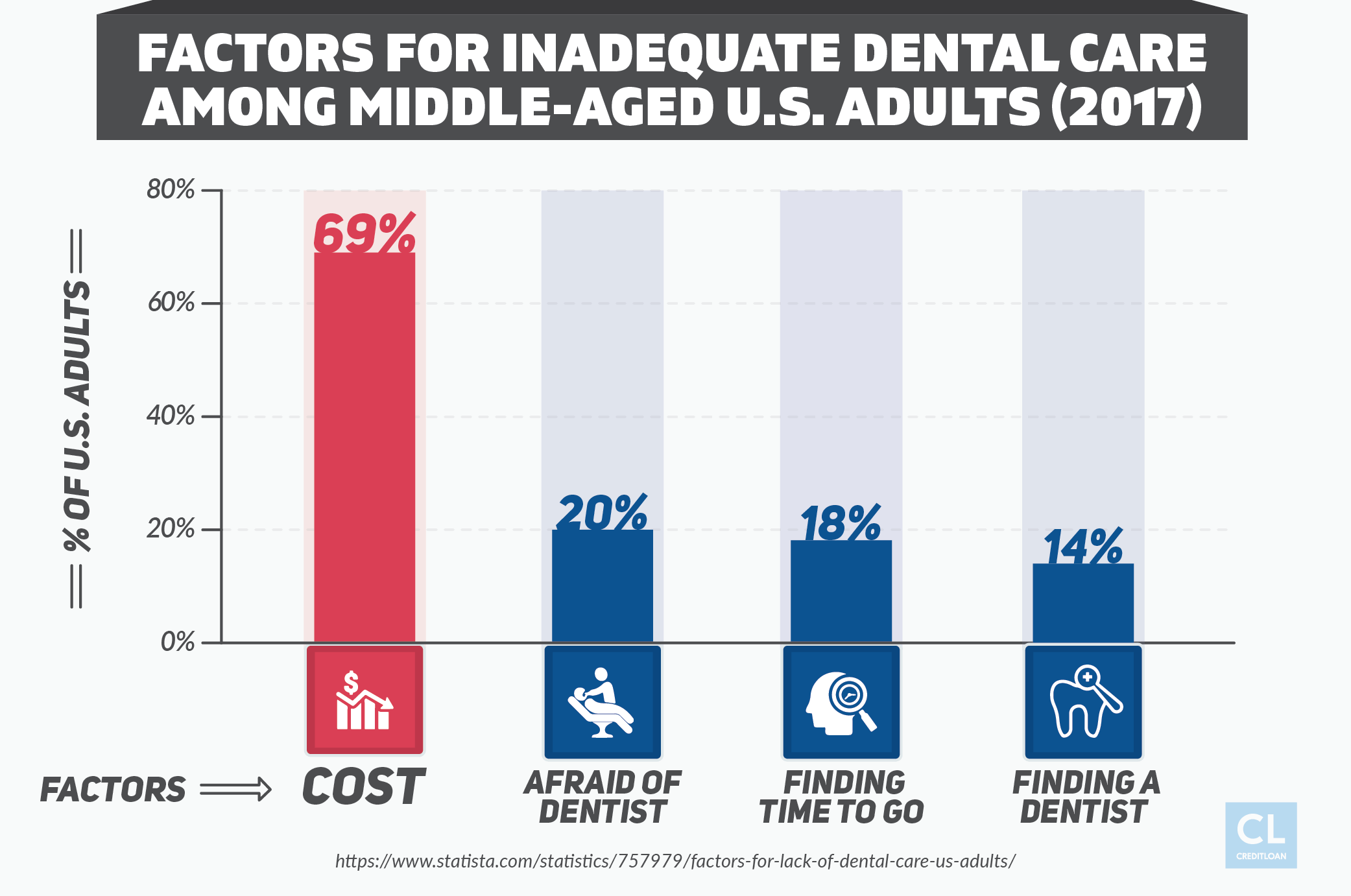

Take care of your teeth!

At least every six months, go for your regular cleanings and exams. Don't wait for the pain. Root canals and crowns can cost anywhere from $1,000 to $3,500! (Painful indeed!)

If you need dental work, don't be afraid to call around and ask for pricing; there can be significant variation between reputable dentists.

"Commit to quit!"

Give up one unhealthy or financially bad habit—smoking, gambling, drinking soda—and methodically put aside the money you would have spent on that habit.

If you're a 4-cigarettes-a-day smoker in New York City, for instance, you'll save morethan $1,000 a year by kicking the habit!

- Find out exactly how much you'll save over a day, week, month, year, even 10 years by using the calculator at SmokeFree or Quitnow.

- Don't think you're off the hook, drinkers. Alcohol costs more than you probably realize.

By placing a higher value on taking care of yourself, you'll subsequently lower your medical care costs and decrease those unhealthy wastes of money you know you feel constantly guilty about. Indeed, taking care of your body is one more way of also taking care of your bank account, both now and down the line.

4. Know your partner's financial history before it costs you

If you blindly combine finances with your partner, you may be putting yourself at significant risk.

Being part of a couple carries significant financial implications down the road, including shared assets, debts, taxes, and so on.

Be as diligent as possible before committing. Make sure you love their mind, body, heart, soul, and—we hate to say it—bank account. Consider these tips:

Think twice before opening joint bank accounts

Even if an account was yours to start, adding a partner's name to the account means he or she can empty it and close it without your permission.

"In some cases, the emptying of the account may happen at the very beginning of the divorce, a kind of preemptive strike meant to deny the other spouse access to money to hire an attorney in the first place. The scary thing is that this happens far more often than you might expect," says attorney J. Benjamin Stevens.

"Be aware of debt you two!"

Full disclosure is important on both sides; will you share each other's debts and income?

If one of you is in a financial hole, is the other one OK with (and capable of) being the breadwinner for an extended time? And if the relationship doesn't work, are you responsible for debts your partner racked up?

Look at paperwork together, check with a financial planner, and be aware of whether or not you're in a community property state—meaning that debts incurred by one spouse during a marriage are also shared by the other spouse, even if they split up.

Choose your partner carefully, not only because it really stinks to be with the wrong person, but also because the financial ramifications can be significant.

5. A life plan can drive you to success

Writing down your goals—whether that's career goals, financial goals, or personal goals–increases the chance of achieving them by 33 percent, according to a Dominican University study.

Consider writing down both short- and long-term goals and reviewing them monthly to check for progress or stalls. Then, get working on these bits of how-to-take-it-one-step-further advice:

Have an accountability partner

The most financially-successful folks are, by far, the people who sent regular progress reports to a friend. It's just human nature!

Andy Hayes at CalculateMyWealth offers tips about what to look for in an accountability partner, as well as what you should agree on in writing: the timing (how and when you'll communicate), the agenda, and your written goals.

Use online tools to plan your financial future

Financial advisors can be expensive, and often don't want to work with low- or middle-income investors. To start your education, explore online financial planning options as recommended by USNews:

- MyFinancialAdvice

- LearnVest

- Jemstep

The more you can articulate your plans in writing and make yourself accountable to someone for following through, and the more you leverage expert advice and apply it to your dollar bill endeavors, the more likely you are to hit your financial goals.

In fact, the American Society of Training and Development reports that the probability of completing a goal if you have a specific accountability appointment with a person is—wait for it—95 percent!

6. Use free budgeting and saving tools

"There's an app for that" isn't a popular phrase for nothing! Truly, budgeting and saving are merely a few clicks away, and services your parents paid big bucks for to financial advisors and the like can be yours for no more than a few bucks via your App Store button.

Consider installing these handy budget helpers:

Wouldn't it be nice to know just how much you can comfortably spend on entertainment before you're risking your bill money without needing to carry a small notebook around with you at all times? Check these out:

- Mint: A robust tool from Intuit for you to link all your financial accounts, track bills and investments, create budgets, and sort your spending.

- Household Budget Worksheet: Kiplinger provides this fill-in-the-blanks online tool to help you see your income and expenses more clearly.

- Acorns: This "microinvesting" tool automatically rounds up your purchases to the nearest dollar and invests the change.

When you're shopping for anything from holiday presents to hotel reservations, you can effortlessly get back a portion of your money just for signing up. Most cover online shopping, but some also link to your credit card for in-person spending:

- Ebates: Install the browser extension, and it'll alert you when you're shopping on a site that offers cash back—then send you a check anytime you've earned more than $5.01 per quarter.

- Favato: This app aims to reduce your grocery bill by showing you the best prices and coupons nearby for the items you're shopping for.

- UPromise: Earn 2.5-5 percent cash back for college on online shopping, restaurants, and travel expenses.

- Honey: This Google Chrome extension searches for coupon codes for you so that you can just click to input them wherever you're shopping, it checks for lower prices, and it offers variable cash back.

Taking just a little bit of time to set up these apps and programs can add up to big-time savings and a better handle on your monthly budget.

7. Make smarter consumer decisions for long-term financial health

Part of being financially wise is also being a smart consumer—comparing prices and plans, analyzing whether or not you need a service, and living within your means. Even the smallest changes and sacrifices can add up to big savings.

Keep these thoughts and questions in mind:

Study your bills

- Are you using the data or minutes your cell plan provides?

- Could you move to a lesser plan?

- Have you compared other carriers' plans lately?

Bundle and bargain

- Among those with "triple play" services (phone, cable, and internet), nearly half of people who called to complain about pricing did get a reduction on their bills. Make that phone call!

Cutting cords

- Who needs cable? Bet you don't.

- Chances are good that if you're 30 or under, you've already cut the cord (or never had one to begin with!), but if you haven't, check into your options at Netflix, Hulu, Playstation Vue, Amazon Prime, and Sling.

- If you still have a landline for your home or business, also look into Ooma Telo, which eliminates your phone bill entirely except for taxes and local fees.

Know what car you can afford.

- Edmunds offers a car calculator that allows you to see what car makes sense for your budget and earnings.

8. Avoid "bad" debt like the plague

Plastic can be so tempting. It's easy to get in over your head with credit cards, spending too much on clothes, concert tickets, restaurants, and vacations because you're sure you'll be able to pay it off later.

The problem is falling behind just a little can snowball until credit card debt gets unmanageable.

Debt in the thousands hanging over your head each month? No, thank you!

Exclude yourself from bar charts like that by keeping up with the right habits. You'll avoid a lot of stress and financial limitations later, trust us! Here are some strategies that can help:

Borrow purposefully

Some things are considered "good debt," such as student loans, for instance

If you took on debt to purchase something that will increase in value and can contribute to overall financial health, you can feasibly consider that to be "good" debt.

On the other hand, anything that depletes your savings without adding potential value is a bad debt (like high-interest credit card debt).

Watch your debt-to-income ratio

Even good investments (a mortgage, business loan, student loan, office equipment, etc.) need to be kept in check.

Irby suggests tallying up your monthly income and total monthly debt. "Your total debt-to-income ratio, considering both good and bad debt, is best at 36 percent or lower."

So if you're earning $4,000 a month, all of your debts should ideally add up to $1440 per month or less.

Plug the holes in your ATM or debit card

Carefully look over the transactions on your last couple of bank statements to see why you're having trouble controlling your balances.

Financial Freedom Now did some serious calculations to find that the average coffee drinker would save $735.84 per year by brewing it at home.

If you're in debt, leave your cards at home—pay with cash except on online purchases.

9. Become one with your credit score

Your credit score is like a letter of reference about your ability to pay back the money you borrow.

It's part report card (how faithfully have you paid your bills on time thus far?) and part projection (how much debt do you have versus how much you're allowed to borrow, how long have you proven yourself, etc.).This is about how much each factor counts:

Not only can you have access to financial products like a mortgage, car loan, etc. if you have a good credit score (which can mean a bigger house, better car, and so on), it also means you can pay less in interest on big stuff, have lower car insurance rates, and find it easier to get approved for an apartment.

What is a good credit score? Each lender has their own viewpoint on what equals "good," but most assert that a credit score of 700 (from a range of 300 to 850) hits the mark.

Maximize your credit score tomorrow by doing these things today (figuratively speaking):

Have one or two credit cards

Your credit score is based on your payment activity and history, so you have to show you can handle credit. Department store cards count, too.

You don't need to use credit cards much—just a purchase or two every few months establishes a credit history.

Ask for higher limits

If you've established that you pay off your balance on time each month, ask your credit card companies for higher limits.

Take it from Shaun Plum at MoneyTips, who writes:

"Few credit card users ask credit card companies to raise their credit limit, but research shows that doing so can help improve their credit scores.

This is because the higher limit improves their credit utilization rate, which is the percentage of credit the consumer is using out of the total credit amount available to him or her.

With a higher limit, that percentage decreases, making the borrower look more appealing to lenders.

Those who have had difficulty qualifying for low-interest rates on auto loans or mortgages may find adjusting their credit utilization rate can help them get the rates they want because it accounts for almost a third of their FICO credit score."

Don't open many accounts in a short time span

MyFico, which provides consumer access to FICO scores, advises, "New accounts will lower your average account age, which will have a larger effect on your scores if you don't have a lot of other credit information. Also, rapid account buildup can look risky if you are a new credit user."

Don't close unused accounts

"Canceling a card can lower your score because it leaves you with less overall credit and instantly raises the percentage of debt capacity you are using. A long credit history is a part of what makes for a high credit score," says Dan Kadlec of CBS MoneyWatch. Feel free to chop up your old credit cards; just don't officially cancel them.

Dispute incorrect or unfair strikes against you

Check your credit report at least once a year and make sure the information is all correct.

If you see an error, don't think it's impossible to correct. It's straightforward to dispute incorrect items:

- Inform the credit reporting company in writing of the error. Use this sample dispute form provided by the FTC.

- And what if the negative item is correct but unfair? What if you didn't pay a bill on time because you were in the hospital, or your house burned down, or…? Try sending a "goodwill letter" to the creditor. Anisha Sekar of NerdWallet suggests, "Your goal is to explain why you missed your payments and why the creditor should wipe them from the report." If this fails and you have a solid reason, you can also try disputing directly with the credit bureaus.

Points earned today are worth lot's of dollars tomorrow

Staying on top of your credit score from the beginning will make it so much easier to get loans at good rates when you need them.

Take this scenario with personal loans:

Let's say you're borrowing $25,000 to help get your small business started.

Show up at the lender's office with a 630-689 credit score, considered "average" by most lenders, and you'll be charged a rate of 19.84%.

That means you'll pay $927 per month to pay that loan back.

But if you waltz in with a 720 score or above, you'll only pay 10.94%, or $818 per month.

Just by having 31 extra points on your score, you can save $109 per month on that loan.

Instead of spending nearly $4,000 in interest over 3 years, you could invest that money in your new business.

10. Hop on the retirement planning bandwagon

What sounds better to you: continuing to work 40 hours a week at 70 years old because you don't have anything saved up, or traveling through Europe at 52 because you were able to retire early?

Even if you are hugely distrustful of the stock market, most professionals agree that an investment portfolio is one of the best ways to have a secure financial future.

In fact, Sheyna Steiner of Bankrate says, "The only way most people have any hope of creating real wealth is by investing in the stock market." You owe it to yourself to at least learn the basics:

School yourself on the basics of investing

- The U.S. Securities and Exchange Commission provides a good debriefing about investing here.

- Or, if you prefer to watch and then chill/invest: William Ackman, the founder and CEO of Pershing Square Capital Management, offers a 45-minute video about investing.

- Mike and Lauren Moyer offer a 5-minute crash course about things like index funds about things like index funds, mutual funds, and stocks.

Watch your dollar grow

- "Millennial Money" author Patrick O'Shaughnessy lays it out: On average, and after accounting for inflation, if you invest $1 in the stock market at age 22, it will be worth $17.70 when you're ready to retire.

Stocks win over bonds or cash

- When your aim is financial growth over a long period, "Historical data clearly shows that common stock and real estate are the only two asset classes that have grown faster than the rate of inflation over time," says Mark P. Cussen of Investopedia.

Once you're in the know, start taking some additional retirement planning action:

If your company offers a 401(k), take it

A 401(k) lets you invest a part of each paycheck into your retirement fund.

Most employers have a matching funds policy, meaning that they kick in extra money to match what you put in, up to a certain cap.

Employers match an average of 4.7 percent of your salary annually, according to the Plan Sponsor Council of America.

It's wise to try to max out your 401(k) contributions each year.

Free money!

Start an IRA account

IRAs (Individual Retirement Accounts) are not employer-sponsored; you have to open one yourself.

You can open an IRA at a bank, brokerage firm, or mutual fund company, and it's up to you how much to invest each year, subject to certain tax caps.

Set realistic goals

Eventually, you should aim to save 12-15 percent of your income for retirement, but Vanguard suggests starting where you can and increasing by 1 percent a year until you hit that mark.

Aside from having guaranteed money to live on when you retire, saving for your retirement now can also offer you tax breaks and help you watch your savings grow effortlessly.

In her article, "Retirement planning for 20-somethings," writer Leslie Haggin Geary presents this encouraging scenario:

If you begin saving for retirement at 25, putting away $2,000 a year for just 40 years, you'll have around $560,000, assuming earnings grow at 8 percent annually.

11. Become a tax filing master—and make Uncle Sam work for you

If you usually get a tax refund, don't think you've suddenly won something. Actually, what you've done is given the government a free loan on money that belongs in your account— earning interest.

On the other hand, if you owe money, you could get hit with penalties.

You want to come as close as you can to zeroing out.

To get to zero, make your accountant or the HR person at your job your new BFF (talk out the best options for you), keeping the following in mind:

Don't mess around with your taxes

Dishonesty can cost you big-time in case of an audit.

Tax evasion is a felony that can lead to fines, penalties, and even jail time.

Even if the IRS decides your failure to file correctly was due to negligence rather than willful evasion, they can still impose a penalty of up to 20 percent of what you the underpayment.

Find ways to minimize your tax bill

Kiplinger offers 71 tips for tax savings, including things like deducting the cost of moving expenses if you had to move more than 50 miles to a new job, or the cost of job-hunting if you were unemployed during the year.

Keep track of what you spend your money on

Seventy percent of Americans just take the "standard deduction," which may be easy, but not smart. Why? Because it doesn't take into account your personal expenses and situation. It simply is the standard amount you can deduct off your income to help lower your tax burden.

More than two million taxpayers overpay their taxes by an average of $610 per year because they don't itemize. You don't want to be overpaying, too.

Keep strong records of your expenses so you can compare and figure out which nets you the best benefit. Check out all the online tools and services.

Keeping track of your tax responsibilities can save you from a financial shock in April, and can stop you from giving the government a free loan.

12. Set up that emergency fund everyone's always talking about (you'll thank yourself later)

Aim to save three to six months' worth of living expenses in a separate account that can't be touched except in true emergencies.

The difference between having this and not could one day save you if you suddenly need surgery, go through a natural disaster, or your car breaks down in the middle of nowhere.

"If you think you don't have any spare cash in your budget to save for an emergency fund, where do you think you'll get the money to pay for an actual emergency? Selling plasma?" asks Cameron Huddleston of Kiplinger.

It's important to save even a few bucks at a time to cover yourself in case of emergencies (they will eventually pop up).

Here are 3 out of 16 great ways you can start filling up your emergency fund today:

Start anywhere

Even saving up two dollars a day will net you $730 at the end of the year—enough to cover an unexpected car repair or medical bill.

Have a measurable goal

"For example, one specific goal may be to save an extra $300 over the next six months to put into an emergency fund," says the Financial Industry Regulatory Authority.

Automate it

Consider setting up an automatic recurring transfer from your checking account into the emergency savings account after every paycheck.

"You might even be able to get your employer to split the direct deposit on your paycheck, putting that money into a separate account automatically," says Amy Podzius at Teachers Insurance and Annuity Association of America.

The Bottom line

The moves you make right now can set you on a great financial path toward the lifestyle you've dreamed about. The more you educate yourself and take charge of your finances, the better the chances you have of living comfortably and retiring young.

Even when they're baby steps, every step you make in the right direction moves you closer to a life free from financial concerns.

5 things you can do today to become financially independent tomorrow

- To take care of your credit score, you have to know it. Request yours. It's free!

- Pay for career training, not just a college degree. Consider a 2-year program.

- Pick a low-fee bank. Set up an automatic transfer from your paycheck to your savings account. Have that savings account link up to an investment account, like an IRA. Invest in a mutual fund that tracks the US stock market, liks SPWWX.

- Sign up for a free budget tracking app, like Mint. Know where your money goes, so you can save it.

- Pick a sport you love. By being active, you'll be less likely to excessively drink and smoke, lowering what you pay in health insurance, medical bills, and increasing your chance to earn more money.

Want more great tips about becoming financially free and secure? Check out these helpful articles:

We're sure you've heard a lot of advice about how to live your life. So far, what's the one tip you wish you hadn't ignored? If you could go back in time and tell yourself something about managing your money, what would it be?

Let us know in the comments below.