Most people these days have some form of college loan debt.

And student loan repayment can feel like a lead balloon constantly holding you down.

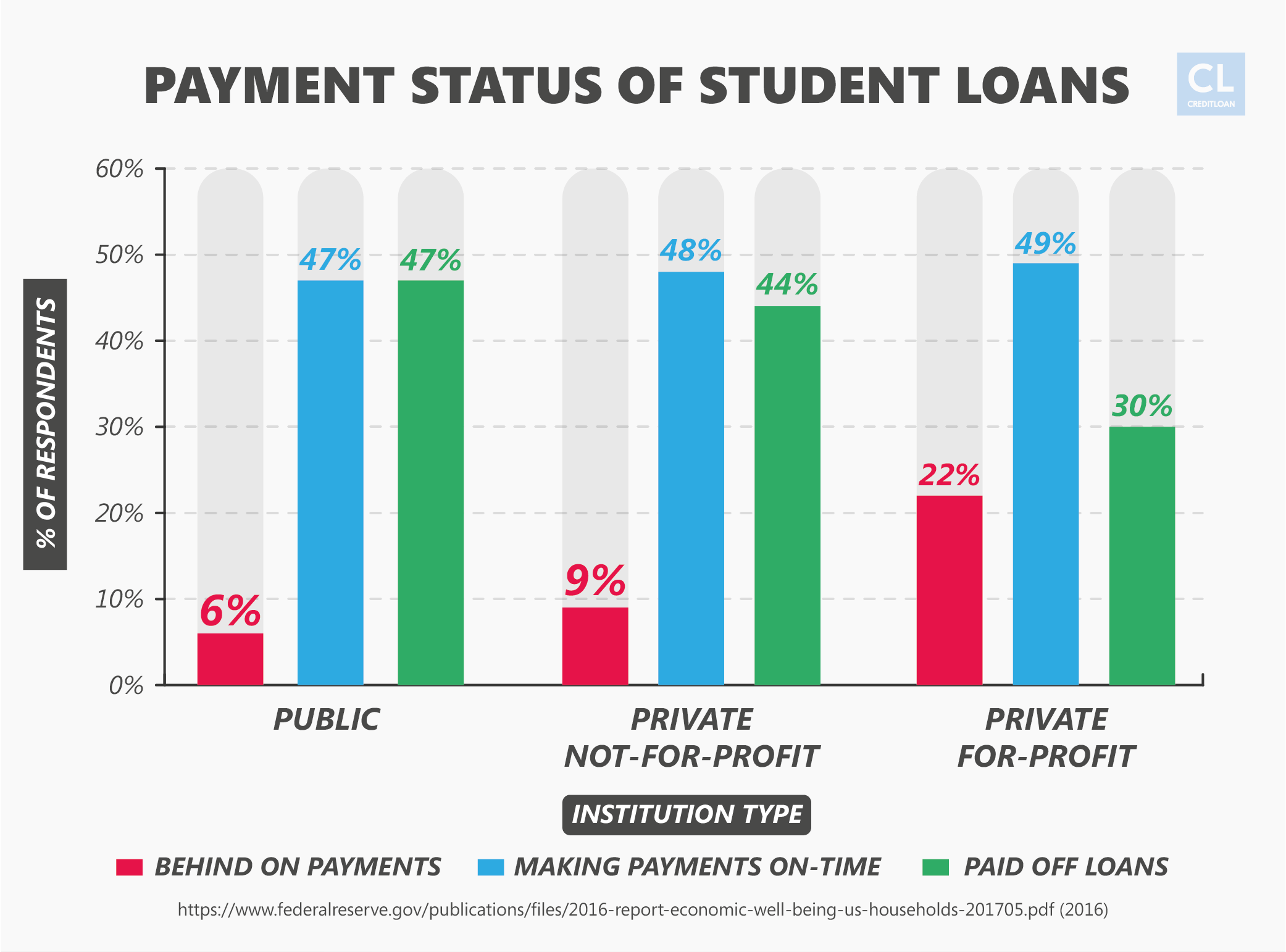

High college loan payments lead to less financial security, with less discretionary income to spend on things like food, fun, and long-term security.

To see just how abysmal student debt can be, let's delve into some stats.

About one-in-five employed adults ages 25-39 with at least a bachelor's degree and outstanding student loans have more than one job, according to the Pew Research Center.

Even more saddening, only 27% of young college graduates with student loans say they are living comfortably, compared with 45% of college graduates of a similar age without outstanding loans.

But there's an often overlooked option to help get yourself out from under that student loan burden: loan forgiveness options.

There are various options for federal student loan holders to have all or a portion of their debt erased, saving them thousands in the process.

Read the list below and get on the path to erasing your student debt and getting on the path to financial freedom.

Public Service Loan Forgiveness

Get a job in public service and dump your student loan debt

If you've been working—or plan to work in—a public-sector job for the previous decade, you can apply to have the remaining balance of your federal student loans forgiven.

You can receive loan forgiveness from the federal government by working for at least 10 years in qualifying fields, such as firefighting, teaching, military, government, and nursing.

5 things you need to know about Public Service Loan Forgiveness

Learn if your job qualifies you. The Public Service Loan Forgiveness program (PSLF program) is open to people working in public service fields who are currently in student loan repayment plans.

You're eligible if you work for employers that include government organizations at any level, not-for-profit organizations that are 501(c)(3) tax-exempt, and AmeriCorps or the Peace Corps.

You must be working full time in your position, which amounts to 30 hours or more per week.

If you work part-time for two different qualifying employers (i.e., a government agency and a not-for-profit) and your combined hours add up to 30, you may still be qualified.

Make qualifying payments. To receive loan forgiveness through the PSLF program, borrowers have to make 120 qualifying payments.

These don't have to be consecutive, though.

Qualifying payments must include all of the following elements:

- Was made after October 1, 2007

- Was made no later than 15 days after due date

- Was for the full amount due

- Was made while working full-time for a qualifying employer

- Was part of an income-based repayment plan (a plan based on your income)

- Was made on a loan serviced under the William D. Ford Federal Direct Loan Program

Consolidate loans to make them eligible. If you received a Federal Perkins Loan or a Family Education Loan (FFEL loan program), your only option for eligibility is to consolidate with a direct consolidation loan.

Note that only payments made towards your direct consolidation loan will count as qualifying payments.

Consider possible changes to the program. The House of Representatives is currently reviewing the PROSPER Act.

The proposed bill will eliminate the Public Service Loan Forgiveness program, starting with loans that originate after 2019.

Apply if you're eligible. Since you have to make 120 qualifying monthly payments, it will be at least 10 years after you make your first qualifying payment before you can apply for Public Service Loan Forgiveness.

It's best practice to complete and submit the Employment Certification for Public Service Loan Forgiveness form annually or when you change employers.

This will let you know that you're making eligible payments.

If you don't submit the form regularly, then you'll have to submit an Employee Certification form for each qualifying employers you worked for when you apply.

Applying for and enrolling in the Public Service Loan Forgiveness program could save you from future student loan payments.

Consider, for instance, that you took out a $30,000 student loan at 6.8% interest (the standard rate on Stafford loans) to be paid out over a 20-year term.

You'd be making a monthly payment of roughly $229. With interest, you'd end up paying a total of $54,960.95.

But if you receive the Public Service Loan Forgiveness, which would save you an extra 120 payments, you'd save more than $27,000 over the next decade.

Stafford Loan Forgiveness Program for Teachers (or Teacher Loan Forgiveness)

If you've been teaching for the past five years, you can save thousands on your student loans

Qualified teachers who have worked five consecutive years in low income and under-served areas of the country can save thousands on their outstanding balance for Direct Subsidized and Unsubsidized Loans and Subsidized and Unsubsidized Federal Stafford Loans.

5 things to know about teacher loan forgiveness

Know if you're qualified. To be considered for teacher loan forgiveness, you must be in repayment of a federal student loan (either a direct or Stafford loan).

Loans made through the Perkins or an FFEL loan program are not eligible.

Also, you must work as a teacher (with all degrees and certifications for the subject/grade level you're teaching) for more than five years in an area short on teachers, or other qualifying areas.

You can check the government's database to see if you're working in a qualifying area.

See how much can be forgiven from your loans. In general, the Teacher Loan Forgiveness program will forgive $5,000–$17,500 from the outstanding balance on your federal student loan.

But, the amount depends on your level of teaching credential as well as what or whom you teach.

You'd be eligible for up to $17,500 if you're a secondary math, science, and special education teacher.

Elementary school teachers and secondary school teachers who teach other subjects can get up to $5,000 forgiven.

Check if your state matches forgiveness amount. If you get approved for loan forgiveness by the federal government, some states will increase your forgiveness amount.

Illinois, for instance, will match your forgiveness amount by up to $5,000.

Apply when you're eligible. After you've completed the required five consecutive years of teaching, apply for loan forgiveness by completing and submitting the Teacher Loan Forgiveness Application to your loan servicer.

Weigh other options. Unless you have a small amount of outstanding debt, the Public Service Loan Forgiveness program could be a better option for most teachers.

Let's look at our previously mentioned loan: a $30,000 student loan at 6.8% interest (the standard rate on Stafford loans) to be paid out over a 20-year term.

The Public Service Loan Forgiveness program could save you more than $27,000—$10,000 more than you'd save through the teacher forgiveness program.

While there is potential to receive forgiveness under both the Teacher Forgiveness program and the PSLF program, you cannot be approved for both during the same period.

Say, for instance, you taught for five years and are accepted for student loan forgiveness under the Teacher Loan Forgiveness program.

Any payments you made for that loan repayment program are not counted towards your 120 qualified payments to receive forgiveness under the PSLF program.

In essence, you'd have to teach for at least 15 years to double-dip.

Obama Student Loan Forgiveness (also known as the Federal Direct Loan Program)

Don't be fooled by companies advertising the Obama Student Loan Forgiveness program

You may see different companies advertising to help you receive loan forgiveness through the Obama Student Loan Forgiveness program.

Ignore these companies.

What you need to know about the Obama Student Loan Forgiveness program

There is no actual program. The Obama Student Loan Forgiveness program is just a nickname for the Federal Direct Loan Program.

That is, it's another name for the program that lends out federal dollars to help you pay for college tuition.

The nickname comes because of Obama-era changes to the loan program that offers more options for loan forgiveness.

Private companies are conning people. A lot of for-profit companies are advertising their services to help borrowers get their loans forgiven.

These services can cost more than $1,000.

The problem?

The actions these companies are helping with are no-cost actions—enrolling borrowers in federal programs for debt relief, such as an income-based repayment plan or the Public Service Loan Forgiveness program.

Forgiveness for Income-Driven Plans

If you tie your repayment plan to an income-based option, you can save thousands of dollars

While not a concrete forgiveness program like the Public Service Loan Forgiveness Program, tying the repayment plan of your loans can lead to significant savings in the long run.

4 things to know about income-driven plans for forgiveness

Choose from income-based options. There are three different options to choose when considering an income-based option:

- Income Contingent (ICR). This option allows you to make payments based on your income, family size, loan balance, and interest rate.

- Income-Based (IBR). In this option, your monthly payments would be limited to just 15% of your discretionary income. Under these plans, borrowers must make monthly payments for 20 or 25 years; you'll also need to update your loan servicer if/and when your income changes.

- Pay As You Earn (PAYE). With this option, monthly payments are limited to just 10% of your discretionary income. Borrowers must make consistent payments for at least 20 years to be considered for loan forgiveness.

Easily apply. If you have any type of federal loan, you can apply for an income-based payment plan by visiting StudentLoans.gov.

Save thousands on interest. If you enter an IBR repayment program, interest is not capitalized (meaning no unpaid interest is added to the total principal balance) on your loan for three years.

That can add up to thousands of dollars in savings.

Let's look at an example: A $40,000 loan with 6.825% interest for a term of 25 years.

The borrower is not married and has an adjusted gross income of $20,000 a year.

The normal interest would be $229.17 per month, but the borrower qualified for an IBR-based payment of $93.69 per month.

That's savings of $135.48 per month, or $4,877.28 for the first three years.

Get your loan balance forgiven at the end of the term. If you enroll in an income-based repayment plan, your outstanding balance would be forgiven at the end of your term.

Consider, for instance, a loan with the following terms: $85,000 student loans with an interest rate of 6.875% over 25 years.

The borrower signs up for an IBR payment plan and qualifies for a monthly payment of $218.69.

The total amount the borrower would pay is $65,607, meaning that's a savings (or forgiveness) of 19,393.

It's worth noting, however, that income-based repayment programs for student debt can be a bit tricky, as they're best for lower-salaried borrowers.

Say, for instance, you get a large raise after five years of working.

Instead of being able to use that extra income as you please, you'll be making much larger payments towards your student loan debt.

While this will help you pay down the debt more quickly, it is definitely a trade-off of sorts.

Perkins Loan Forgiveness

If you work full-time in public interest jobs, you can contact your school to have your Perkins loans forgiven

Borrowers who still owe balances on their Perkins loans can have their debt partially or fully erased if they work full-time in a public service job.

This loan option was eliminated on September 30, 2017, after Congress failed to renew it.

You can still, however, apply for forgiveness if you qualify.

What to know about Perkins Loan Forgiveness

How to qualify. In as early as your first year in a full-time public position, you can apply to have a percentage of your loan balance forgiven.

You'll qualify if you're in the following fields:

- Public school teacher

- Nurse or medical technician

- Firefighter

- Provider of early intervention services for the disabled

- Faculty member at a tribal college or university

- Librarian with a master's degree

- Speech pathologist with master's degree

- Law enforcement or corrections officer

- Attorney employed in a federal public or community defender organization

- Military service

How much debt you can have erased. While you can have up to 100% of your Perkins Loan debt erased after five years of work, you don't have to wait five years to be forgiven:

- Get 15% of the original principal loan amount forgiven for each of the first and second years

- Get 20% of the original principal loan amount forgiven for each of the third and fourth years

- Get 30% of the original principal loan amount forgiven for the fifth year.

How to apply. Because Perkins loans are given to you by your college (as opposed to the government), you need to go through the school to receive forgiveness on your loans.

It's best for you to call the financial aid office at the school to ask about the application process.

Since the Perkins Loan Forgiveness option applies to many of the same categories as the PSLF Program, it could be a better choice than applying for a direct consolidation loan to try and become eligible for the PSLF option.

If you're under substantial pressure due to student loans, check your options for debt relief

Student loan debt can keep you financially hamstrung.

But luckily, government loans come with a plethora of options for you to have most or all of your debt erased and can get you on the road to financial security.

Have you ever had your student loan forgiven?

What worked and what didn't?

Any great tips (or nightmares) to share with the rest of us?

Let us know in the comments below.